In monotone comparative statics, the single-crossing condition or single-crossing property refers to a condition where the relationship between two or more functions[note 1] is such that they will only cross once.[1] For example, a mean-preserving spread will result in an altered probability distribution whose cumulative distribution function will intersect with the original's only once.

The single-crossing condition was posited in Samuel Karlin's 1968 monograph 'Total Positivity'.[2] It was later used by Peter Diamond, Joseph Stiglitz,[3] and Susan Athey,[4] in studying the economics of uncertainty.[5]

The single-crossing condition is also used in applications where there are a few agents or types of agents that have preferences over an ordered set. Such situations appear often in information economics, contract theory, social choice and political economics, among other fields.

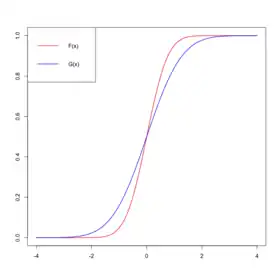

Example using cumulative distribution functions

Cumulative distribution functions F and G satisfy the single-crossing condition if there exists a such that

and

;

that is, function crosses the x-axis at most once, in which case it does so from below.

This property can be extended to two or more variables.[6] Given x and t, for all x'>x, t'>t,

and

.

This condition could be interpreted as saying that for x'>x, the function g(t)=F(x',t)-F(x,t) crosses the horizontal axis at most once, and from below. The condition is not symmetric in the variables (i.e., we cannot switch x and t in the definition; the necessary inequality in the first argument is weak, while the inequality in the second argument is strict).

Use in Social Choice

In the study of social choice, the single-crossing condition is a condition on preferences. It is especially useful because utility functions are generally increasing (i.e. the assumption that an agent will prefer or at least consider equivalent two dollars to one dollar is unobjectionable).[7]

Specifically, a set of agents with some unidimensional characteristic and preferences over different policies q satisfy the single crossing property when the following is true:

If and or if and , then

where W is the indirect utility function.

An important proposition extends the median voter theorem, which states that when voters have single peaked preferences,[8] a majority rule system has a Condorcet winner corresponding to the median voter's most preferred policy. With preferences that satisfy the single-crossing property, the most preferred policy of the voter with the median value of is the Condorcet winner.[9] In effect, this replaces the unidimensionality of policies with the unidimensionality of voter heterogeneity.

In this context, the single-crossing condition is sometimes referred to as the Gans-Smart condition.[10][11]

Use in Mechanism Design

In mechanism design, the term single-crossing condition (often referred to as the Spence-Mirrlees property for Michael Spence and James Mirrlees, sometimes as the constant-sign assumption[12]) refers to the requirement that the isoutility curve for agents of different types cross only once.[13] This condition guarantees that the transfer in an incentive-compatible direct mechanism can be pinned down by the transfer of the lowest type. This condition is similar to another condition called strict increasing difference (SID).[14] Formally, suppose the agent has a utility function , the SID says we have . The Spence-Mirrlees Property is characterized by .

See also

Notes

References

- ↑ Athey, S. (2002-02-01). "Monotone Comparative Statics under Uncertainty". The Quarterly Journal of Economics. 117 (1): 187–223. doi:10.1162/003355302753399481. ISSN 0033-5533. S2CID 14098229.

- ↑ Karlin, Samuel (1968). Total positivity. Vol. 1. Stanford University Press. OCLC 751230710.

- ↑ Diamond, Peter A.; Stiglitz, Joseph E. (1974). "Increases in risk and in risk aversion". Journal of Economic Theory. Elsevier. 8 (3): 337–360. doi:10.1016/0022-0531(74)90090-8. hdl:1721.1/63799.

- ↑ Athey, Susan (July 2001). "Single Crossing Properties and the Existence of Pure Strategy Equilibria in Games of Incomplete Information". Econometrica. 69 (4): 861–889. doi:10.1111/1468-0262.00223. ISSN 0012-9682.

- ↑ Gollier, Christian (2001). The Economics of Risk and Time. The MIT Press. p. 103. ISBN 9780262072151.

- ↑ Rösler, Uwe (September 1992). "A fixed point theorem for distributions". Stochastic Processes and Their Applications. 42 (2): 195–214. doi:10.1016/0304-4149(92)90035-O.

- ↑ Jewitt, Ian (January 1987). "Risk Aversion and the Choice Between Risky Prospects: The Preservation of Comparative Statics Results". The Review of Economic Studies. 54 (1): 73–85. doi:10.2307/2297447. JSTOR 2297447.

- ↑ Bredereck, Robert; Chen, Jiehua; Woeginger, Gerhard J. (October 2013). "A characterization of the single-crossing domain". Social Choice and Welfare. 41 (4): 989–998. doi:10.1007/s00355-012-0717-8. ISSN 0176-1714. S2CID 253845257.

- ↑ Persson, Torsten; Tabellini, Guido (2000). Political Economics: Explaining Economic Policy. MIT Press. p. 23. ISBN 9780262303668.

- ↑ Gans, Joshua S.; Smart, Michael (February 1996). "Majority voting with single-crossing preferences". Journal of Public Economics. 59 (2): 219–237. doi:10.1016/0047-2727(95)01503-5.

- ↑ Haavio, Markus; Kotakorpi, Kaisa (May 2011). "The political economy of sin taxes". European Economic Review. 55 (4): 575–594. doi:10.1016/j.euroecorev.2010.06.002. hdl:10138/16733. S2CID 2604940.

- ↑ Laffont, Jean-Jacques; Martimort, David (2002). The theory of incentives : the principal-agent model. Princeton, N.J.: Princeton University Press. p. 53. ISBN 0-691-09183-8. OCLC 47990008.

- ↑ Laffont, Jean-Jacques; Martimort, David (2002). The theory of incentives : the principal-agent model. Princeton, N.J.: Princeton University Press. p. 35. ISBN 0-691-09183-8. OCLC 47990008.

- ↑ Frankel, Alexander (2014-01-01). "Aligned Delegation". American Economic Review. 104 (1): 66–83. doi:10.1257/aer.104.1.66. ISSN 0002-8282.